What Legal Document To Guarantee Money Owed Template

A loan understanding is a legal contract between a borrower and a lender. Information technology establishes how much coin is existence borrowed and sets other terms of the loan, including the repayment schedule and interest, if applicable.

You should utilise loan agreements any fourth dimension you lend or infringe money, with or without involvement. This includes:

- Lending or borrowing money inside your family

- Lending or borrowing money among your friends

- Borrowing money from an establishment to finance a home, car, or university tuition

- What Is a Loan Agreement?

- Who Needs a Loan Agreement?

- When To Apply a Loan Agreement

- How To Write a Loan Agreement

- Loan Agreement Sample

- Loan Agreement Frequently Asked Questions

What Is a Loan Agreement?

A loan agreement is a written contract between two parties — a lender and a borrower — that tin exist enforced in court if ane political party does not hold upwards their stop of the bargain.

The borrower agrees that the borrowed money will be repaid to the lender at a future date, often including interest. In exchange, the lender can't change their heed and make up one's mind not to lend them coin, especially if the borrower relies on the lender'south promise and makes a buy expecting that they'll receive the loan.

A loan agreement is sometimes called:

- Concern loan understanding

- Loan contract

- Personal loan

- Promise to pay

- Secured/unsecured notation

- Term loan

What's the Difference Between a Loan Understanding, Promissory Note, and IOU?

A loan agreement is generally more formal and less flexible than a promissory note or IOU. This agreement is typically used for more circuitous payment arrangements and often gives the lender and borrower more protections such equally borrower representations, warranties, and covenants.

In a loan agreement, a lender tin usually also accelerate the loan if the borrower defaults. So if the borrower misses a payment or goes bankrupt, the lender can make the entire amount of the loan plus any interest due and payable immediately.

Here is a simple nautical chart explaining the difference betwixt an IOU, a promissory note, and a loan agreement.

| Loan | Promissory Note | IOU |

|---|---|---|

| hope to repay | promise to repay | promise to repay |

| steps for repayment | steps for repayment | |

| timeline to repay | timeline to repay | |

| legally binding | legally binding | |

| signature of borrower | signature of borrower | |

| signature of lender | ||

| repay in installments | ||

| consequences of defaulting (i.e. right to foreclosure) |

You can view our article on the differences between the three most common loan forms for more detailed data.

How Will the Coin Exist Repaid?

The loan agreement should particular how the borrower will pay the money back and what happens if the borrower cannot repay.

In that location are by and large 4 types of repayment options:

| Installment Payments | Installments with Terminal Balloon Payment | Due on Specific Appointment ("Lump Sum") | Due on Demand ("Payable on Demand") |

|---|---|---|---|

| Specific due date | Specific due appointment | Specific due date | No specific due date |

| Payments for principal and interest are made at regular intervals | Payments for interest only are made at regular intervals, primary amount due on maturity appointment | Unabridged amount owed, including interest, is paid all at in one case | Unabridged amount owed is due whenever the lender wants his or her money back |

| Example: $1,500 monthly payment really consists of $500 towards the outstanding principal and $1,000 towards the interest with $1,500 due on the maturity engagement | Instance: $500 monthly payment is applied merely towards interest and full $10,000 loan corporeality is due on the maturity engagement | Example: $10,000 loan for a friend's small business is due on a specific date | Example: $10,000 loan for a friend's small-scale business is due at any time or whenever financially viable |

Types of Loan Agreements

There are many dissimilar types of loan agreements, including:

Co-sign Loan

If you co-sign a loan for someone else, such as your spouse or child, y'all'll exist as responsible for repaying the loan. The lender can approach you for repayment if they cannot collect a payment from the borrower.

Fixed-rate Loan

A fixed-rate or term loan has an interest rate that stays the same for the entirety of the loan'due south term. Your lender sets the interest rate when issuing your fixed-rate loan. For example, a 30-year stock-still-rate mortgage at 4% maintains the aforementioned involvement charge per unit for the whole thirty-twelvemonth period.

Secured Loan

Secured loans are personal or business loans that require collateral as a precondition for borrowing, typically a dwelling house or vehicle. If you lot stop making payments on the loan, the lender can seize the property you used to secure the loan. For example, the bank can showtime a foreclosure proceeding in a mortgage loan by auctioning off your home and using the proceeds to repay the remaining amount.

Common examples of secured loans include:

- Life insurance loans

- Vehicle loans

- Mortgages

- Secured credit cards

- Car title loans

- Bad credit loans

Unsecured Loan

In dissimilarity to secured loans, unsecured loans don't crave collateral and are simply backed by a contract. This kind of agreement results in less paperwork and faster approvals. However, it may be difficult to obtain an unsecured loan if y'all don't have a adept credit score. You may too have to pay a higher interest charge per unit for unsecured loans.

Ane of the most popular types of unsecured contracts is a signature loan. Also known as a graphic symbol loan or good faith loan, a signature loan requires only your signature and a promise to pay. Other examples of unsecured loans include almost credit cards and pupil loans.

Variable-rate Loan

Variable-rate loans take involvement rates that change over fourth dimension. However, their rates may be stock-still for a few years at the beginning of the loan.

The underlying index or interest charge per unit for variable rates depends on what security or loan yous accept, but it's about unremarkably based on the federal funds rate or the London Interbank Offered Rate.

2. Who Needs a Loan Understanding?

While loans can occur between family members – called a family loan agreement – this form tin besides be used between two organizations or entities conducting a business human relationship.

Hither is a table detailing mutual borrowers and lenders who might need this understanding:

| Possible Lender | Possible Borrower |

|---|---|

| Seller of a home | Buyer of a habitation |

| Seller of a automobile | Buyer of a car |

| Investor | Startup company |

| Family member | Family unit member |

| | |

| | |

| Sympathetic friend with actress funds (i.e. able to lend but non requite money) | Reliable friend with unexpected debt (i.e. unforeseen medical bills) |

When To Apply a Loan Agreement

You should use a written loan agreement whenever yous lend or borrow money.

Relying but on a exact hope is frequently a recipe for one person getting the short cease of the stick. If the payback terms are complicated, a written agreement allows both parties to conspicuously spell out whatsoever installment payment terms and the exact amount of involvement owed.

If one party does not fulfill their side of the deal, having this agreement in writing has the added benefit of recording both parties' understanding of the consequences involved.

If a disagreement arises later, a loan understanding serves equally show to a neutral tertiary party like a judge who tin can help enforce the contract.

Here are some situations where you may demand a loan understanding:

- Starting a business with a majuscule loan

- Purchasing land or a home with a existent estate loan

- Investing in a college education or repaying a student loan

- Buying a new car or gunkhole

- Getting a paycheck advance from an employer

- Helping a friend or family fellow member out with a personal loan

When making a loan understanding contract between family members, y'all should be aware that in that location can exist taxation implications. For case, if you lend money without interest and so the IRS may charge you taxation because information technology would exist below the minimum interest charge per unit required for family loans. This is commonly known as the Applicable Federal Rate (AFR).

Too, if you're borrowing money from family or friends and you aren't expected to pay the loan back, the IRS will consider the loan as a gift and charge y'all income tax.

Loan agreements can as well assistance you determine which lenders to avoid. People or institutions who lend money at high interest rates may be loan sharks. Loan sharks use predatory loan tactics to charge high rates, leading to a roughshod debt cycle.

What Happens If I Don't Accept a Loan Agreement?

A elementary loan agreement details how much was borrowed, as well every bit whether interest is due and what should happen if the coin is not repaid.

Here is a chart of some of the preventable suffering a loan agreement could foreclose:

| Lender | Borrower |

|---|---|

| Borrowed money unpaid | Unpaid bills |

| Loss in value of used house or auto | Paid for a house or car with no proof |

| Pay the IRS a gift tax of up to twoscore% | Pay the IRS income tax on the "gift" |

| Expensive lawyer fees to: | Expensive lawyer fees to: |

| | |

| | |

| | |

| Loss of friendship or family trust | Loss of friendship or family unit trust |

| Personal safety & well being | Personal rubber & well being |

How To Write a Loan Understanding

Here'southward a step-by-step on how you can write a elementary Loan Agreement with a free Loan Understanding template.

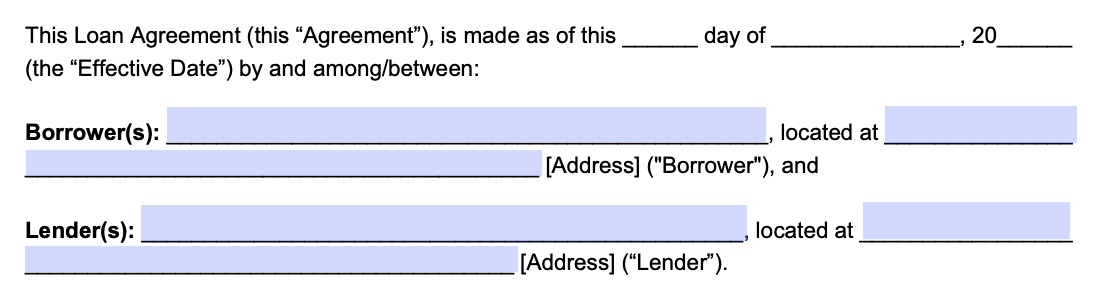

Pace i – Proper noun the Parties

A Loan Agreement should detail the name of the lender and borrower. It should include their legal proper name, not informal designations or "nicknames." This legally identifies the parties involved in the loan, so a proper legal designation of the parties is essential. The initial department of your understanding should look like this:

Footstep 2 – Write Down the Loan Amount

Provide the amount you lot volition be loaning the borrower. This amount is referred to as the 'primary sum'. It does non have into account the total corporeality including involvement.

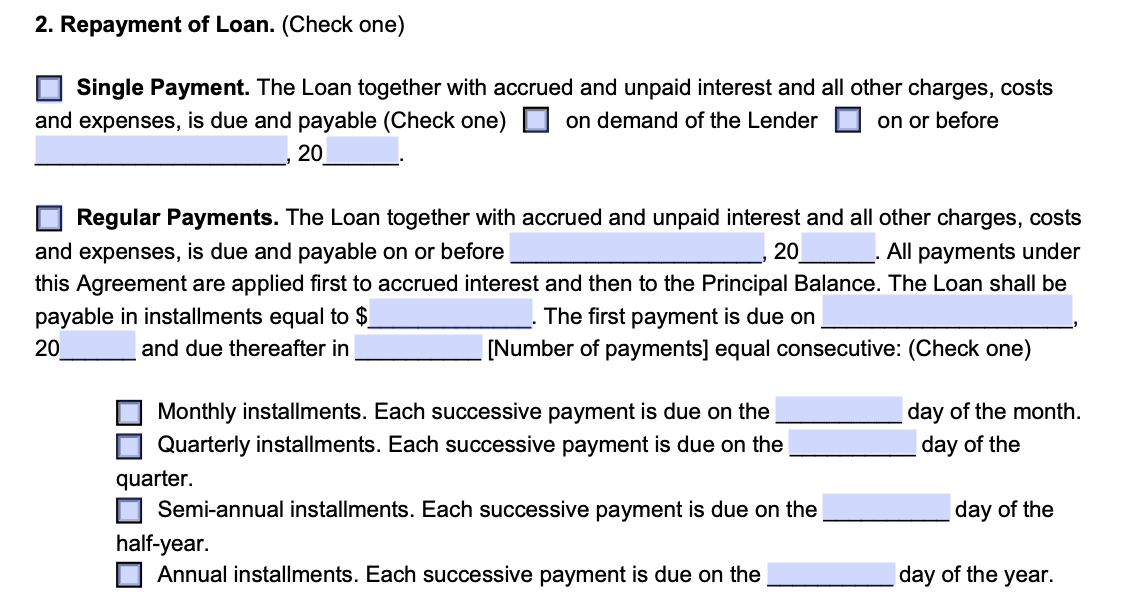

Step iii – Specify Repayment Details

This section is where you will take to provide the details of the borrower's loan repayment. The options you cull will have to be mutually agreed upon. You can choose whether the loan will be repaid in regular payments or all at one time.

Regular Payments: The borrower repays the lender in a set number of payments over a set period of time as specified in the document.

Unmarried Payment: The borrower repays the lender all at one fourth dimension by the engagement that is specified past the lender OR "on demand" past the lender. With a "Due on Demand" payment option, the borrower repays the unabridged loan upon the need of the lender.

If you choose regular payments, you accept to specify the repayment schedule, which can be monthly, quarterly, semi-annual or almanac installments.

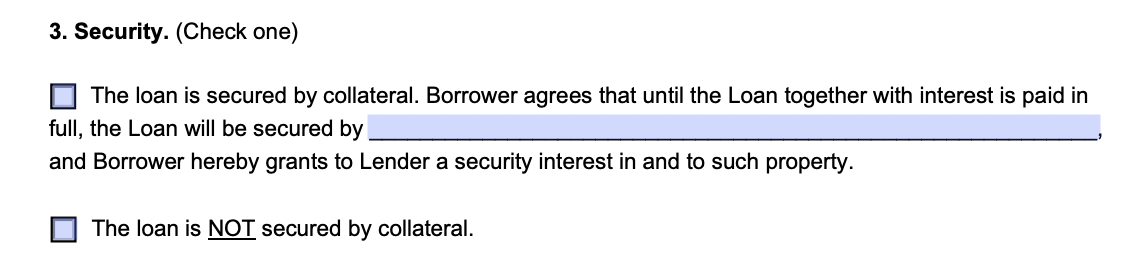

Step iv – Choose How the Loan Will Be Secured (Optional)

If you would like the loan to be secured, you can include what belongings the borrower has put upwardly for collateral hither. Make sure you are specific, providing as many relevant details as possible. This property also has to be mutually agreed upon past both parties for it to be legally valid in court.

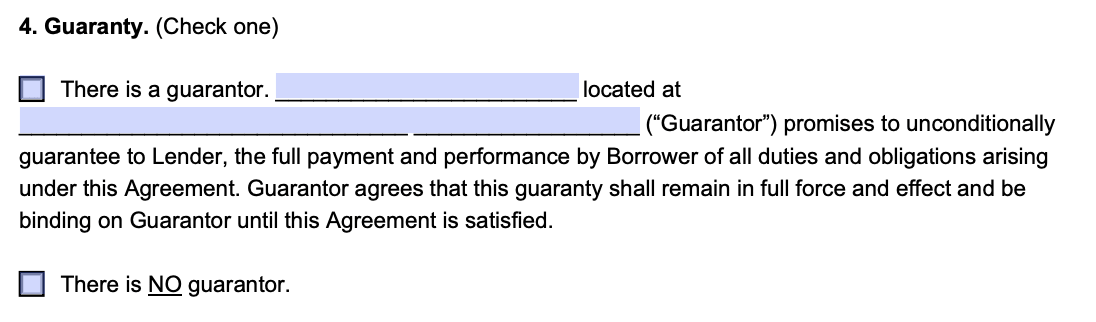

Footstep v – Provide a Guarantor (Optional)

A cosigner or guarantor is optional and protects the lender in case the borrower defaults on the Loan Agreement. You may require a cosigner if the borrower is in questionable financial standing. The cosigner is someone who jointly signs the understanding with the borrower.

In case the borrower defaults and cannot pay back the amount in full, the cosigner is responsible for paying you back the amount due. The cosigner is unremarkably someone in skillful fiscal standing or has excellent credit.

Step 6 – Specify an Involvement Rate

You should include the interest charge per unit you will exist charging the borrower in a percentage. This interest rate will exist applied to the main amount of the loan, and it is important that this charge per unit is agreed upon by the borrower.

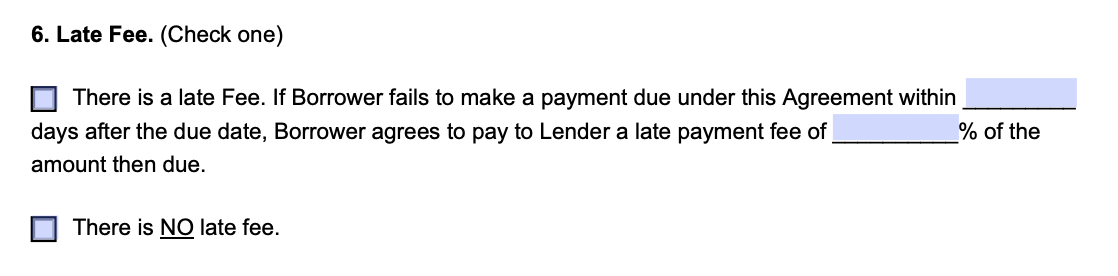

Footstep 7 – Include Late Fees (Optional)

As a lender, you have the option to charge late fees if the borrower does not meet a payment in time. Including a late fee can exist a motivator for the borrower to make their payments on the agreed dates.

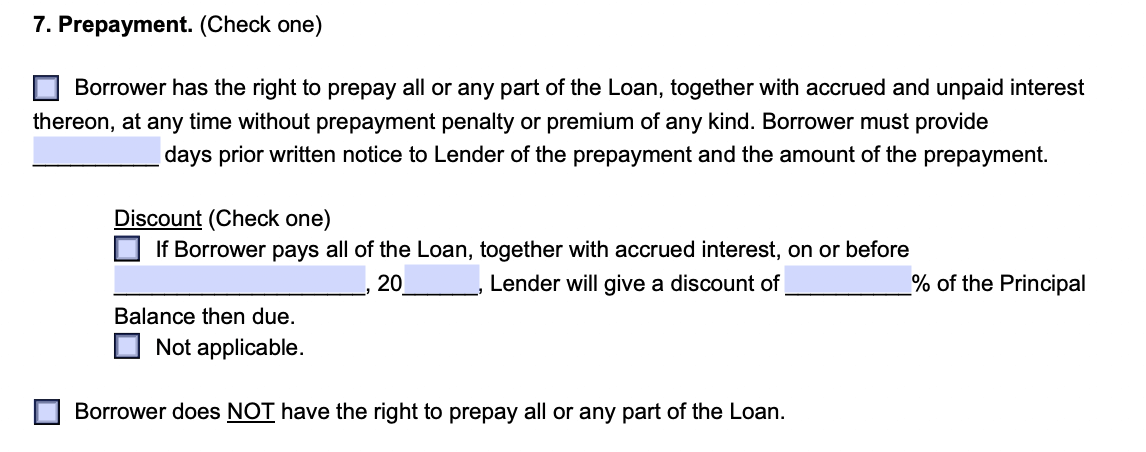

Footstep eight – Determine Options for Prepayment

Y'all tin include whether penalties or discounts will exist applied if the borrower decides to pay the loan amount ahead of schedule. Alternatively, you can explicitly country that prepayment of the loan is not allowed in the agreement.

A punishment is usually applied to deter the borrower from paying the loan back early and to encourage long-term payments. The loan would then accrue more than interest, which can be a favorable arrangement if you're the lender.

Footstep 9 – Include Provisions for a Default

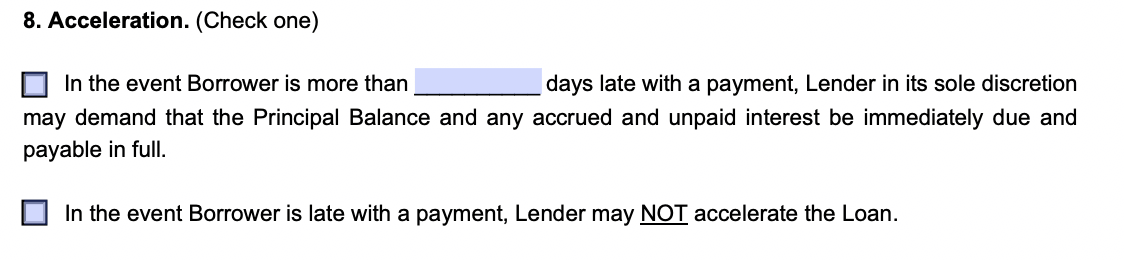

When the borrower is unable to pay back the loan as detailed in the loan agreement, the borrower has entered into default. You should clarify how the borrower will default in the document. Loan agreements tin can say missing one payment causes a default, but equally a lender, you can be more lenient with the terms.

Defaulting on a loan tin give y'all the legal right to advance payment. In this scenario, you can make the full amount of the loan due immediately.

Step ten – Add in Relevant Terms

Farther terms brand upwardly the residuum of the loan agreement and serve to protect the rights of both parties and they include provisions such as:

- The legal right for the lender to enforce the terms of the agreement

- The costs and expenses associated with taking the case to court

- The transferability of the loan agreement

- The capability of alterations to the understanding

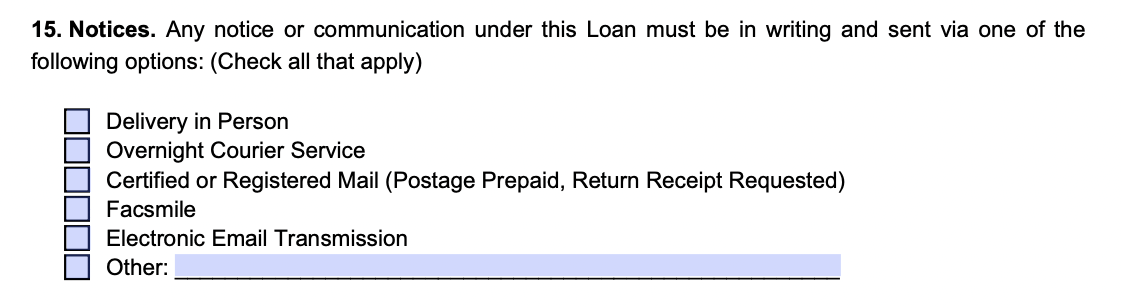

Footstep xi – Specify How You Would Like To Communicate

You tin can institute advice methods for yourself and the borrower and so both parties are on the same page. This avoids either party claiming that they didn't receive a find.

Footstep 12 – Include Your Resident Land

Clearly point your resident state in the loan understanding then both parties are aware of which state or jurisdiction laws they accept to follow.

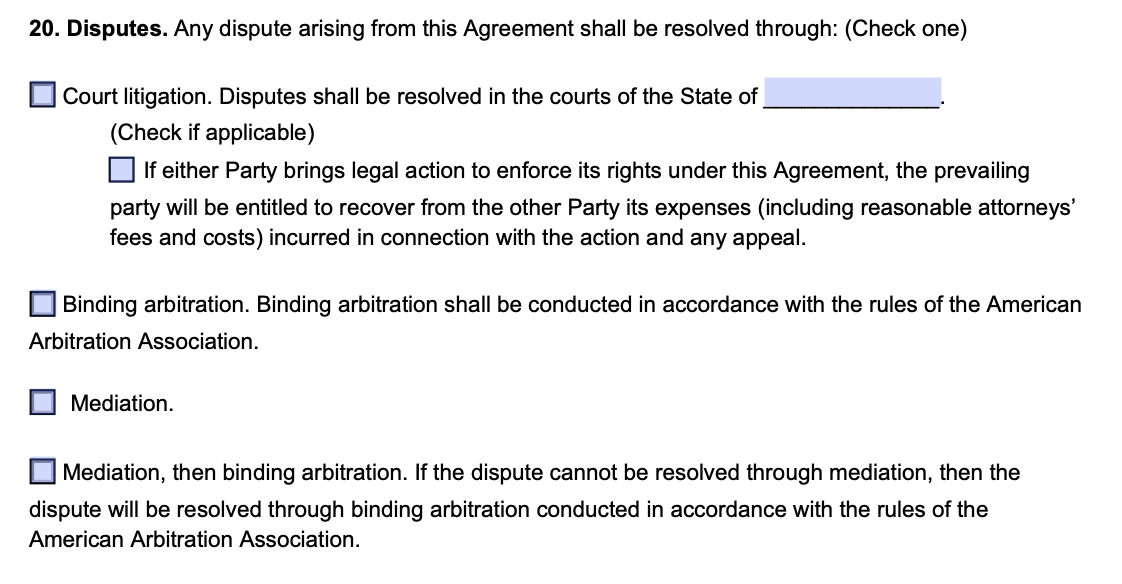

Stride 13 – Decide How Disputes Volition Be Resolved

Detail the process for how both parties can resolve any disagreements. There are numerous options bachelor, ranging from court litigation to mediation. Keep in mind that pursuing courtroom litigation volition mean the party who lost the court instance will accept to pay the other party any costs and fees related to the courtroom procedure.

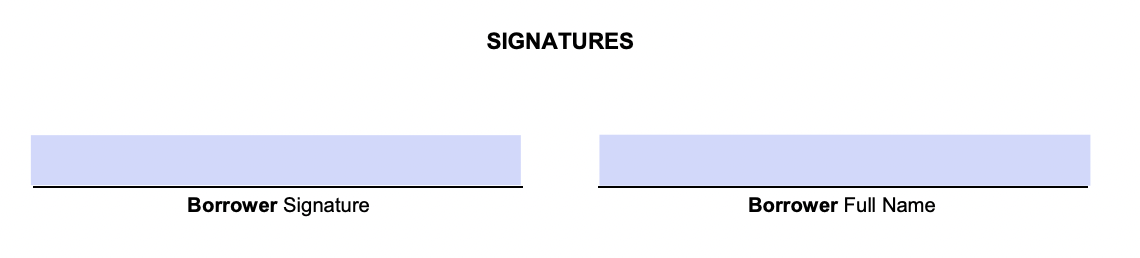

Step 14 – Include All Relevant Signatures

The parties involved in the loan agreement should sign the agreement. This includes any personal guarantors or co-signers.

What Should Be Included in a Loan Understanding?

You should always include the post-obit in your loan understanding:

Basic elements

- Borrower: (aka the "buyer" or "payer") who is receiving the loan from the lender and is responsible for repaying the debt

- Lender: (aka the "issuer", "maker", "payee", or "seller") who is giving the borrower money and receive the repayment

- Principal amount: the sum of money existence borrowed

- Interest: additional money owed, usually a per centum, based on the amount borrowed and fourth dimension until repayment

- Maturity date: when the coin should be repaid

Other details

The contract may besides include these provisions:

- Acceleration: whether the lender can move up the date of repayment or make the borrower repay the loan immediately. Possible events of acceleration include:

- If the borrower becomes bankrupt

- If the borrower fails to brand payments

- If the borrower passes away or the visitor dissolves

- If the borrower wants to pay off the note early

- If the borrower sells off a big or material portion of their assets

- Amendment: whatever changes to the agreement, which must be in writing

- Collateral: what property the lender can go along if the borrower defaults

- Governing police force: which country laws apply if there is a problem with the agreement

- Joint and several liability: states that all of the borrowers are individually responsible for the total amount of the loan

- Late charges: states that the borrower pays a penalty if payment is late

- Prepayment: allows the borrower to pay off the loan and interest early on, mayhap for a disbelieve

- Right to transfer: allows the lender to transfer the loan to another political party

Loan Agreement Sample

Our loan agreement template addresses the following details:

- Who: the borrower and the lender, or the person taking money and the person giving coin

- What: the amount of coin — or chief — that is existence borrowed, and whether interest or a percentage of the principal is also owed

- When: the appointment or timetable that the principal and any involvement should be paid back to the lender

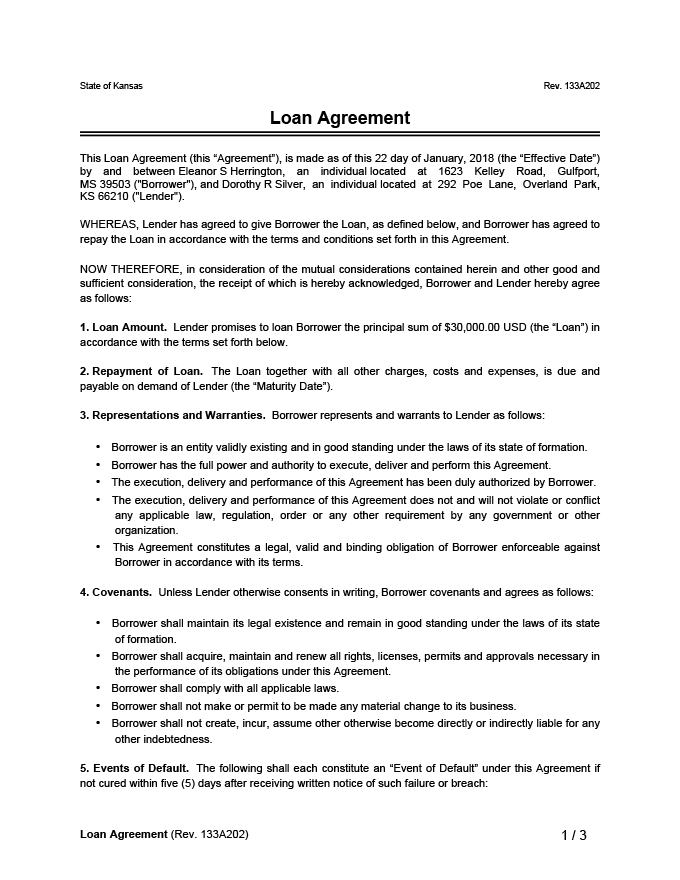

Loan Agreement

Loan Agreement Oft Asked Questions

Does a personal loan agreement need to be notarized?

It's non necessary to notarize a personal loan understanding. However, you may want to notarize the certificate if it involves a big sum. Notarization will help testify the document'southward validity if it'south challenged in court.

Is a personal loan understanding legally bounden?

Yes, a personal loan agreement is legally bounden. Whether the lender is a fiscal institution or an individual, the court volition uphold the terms of the loan equally long as both parties sign the agreement.

If you are the borrower, it is crucial to brand sure you lot tin can repay the loan, as the lender will accept the right to sue you in court for the amount owed. If you cannot pay the lender back, you volition take to provide other means of compensation, such equally giving up some of your assets or having your wages garnished.

Can you cancel a loan agreement?

Yes, in sure instances, yous can cancel a loan agreement. There should be a section on termination in the document's terms and conditions. Information technology should provide you lot with everything y'all need to know virtually how you can go out of the contract.

What Legal Document To Guarantee Money Owed Template,

Source: https://legaltemplates.net/form/loan-agreement/

Posted by: burbankcolooter.blogspot.com

0 Response to "What Legal Document To Guarantee Money Owed Template"

Post a Comment